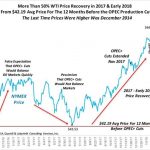

After a 7-month period of remarkably low volatility in the global crude oil markets, the last two weeks have seen a return of turbulence. The sudden correction that has hit stock markets around the world has in turn diminished stability where crude is concerned. A 10 percent drop in the Dow Jones Industrial average was met by a 10 percent drop in the price for WTI, as a strengthening dollar, a jump in the U.S. rig count and the preliminary announcement by the U.S. Energy Information Administration (EIA) that domestic production set a new record of 10.25 million barrels of oil per day during the final week in January led to a predictable reaction in the trader and investor communities.

Suddenly, those $55 hedge contracts some U.S. producers entered into during Q4 2017 aren’t looking so conservative after all , as it appears that the WTI price could approach that level by the end of February. But the question that keeps nagging at my mind is, are we overreacting just a little bit here? True, we’ve had a confluence of seemingly bearish signals in the last two weeks, but it’s hard to keep from wondering how much of it is actually more than offset by other, bullish signals, and how much of it might not even be real?

Let’s take the rig count as an example of a seemingly bearish signal that might not in fact even be real. Last Friday, within a couple of hours after Baker Hughes release its weekly rig count indicating a very large, 29-rig increase in a single week, the WTI price dropped by $2 per barrel,not a surprising reaction when the price had already been in a fall over the 10 previous trading days…